UPI

From Click to Cash: The Complete Saga of How UPI Works & Enhances Lives!

Dive into the digital revolution with our comprehensive guide on “How UPI Works” – uncovering the seamless journey of UPI transactions from initiation to confirmation. Discover the technology, security, and future innovations that make UPI a cornerstone of India’s financial landscape.

Introduction- How UPI Works?

In a world swiftly moving towards digitalization, India has not just kept pace but has leapt with its Unified Payments Interface (UPI) – a system that has revolutionized the way Indians think about and handle money.

At the heart of this revolution lies a simple yet profound question: What happens when you hit the “Pay Now” button? The curiosity surrounding this action opens up a world of digital transactions, seamless payments, and financial inclusion, making “How UPI works” a topic of both national and international intrigue.

Table of Contents

1. Understanding UPI – India’s Financial Marvel

The story of UPI’s inception is nothing short of remarkable. Launched in 2016 by the National Payments Corporation of India (NPCI), UPI quickly became the backbone of the country’s digital payment ecosystem. It’s fascinating to see how UPI allows instant money transfers through mobile devices, making it a marvel in India’s financial landscape.

The growth trajectory of UPI is a testament to its efficiency, with billions of transactions processed monthly. By reshaping Indian transactions, UPI has simplified payments and heralded a new era of financial freedom and inclusion.

2. The Prelude – Initiating a UPI Transaction

The role of UPI apps in facilitating payments is unparalleled. These apps act as a bridge between the user and the complex world of banking, all while maintaining a facade of simplicity.

Initiating a UPI transaction is as simple as clicking the “Pay Now” button from a UPI app like PayTM, GPay or PhonePe, but the technology and processes that kick into gear thereafter are anything but. This step marks the entry into a seamless payment process, illustrating the ease with which “How UPI works” translates into convenience and speed for millions of users.

3. The Digital Handshake – Verifying Account Details

The understanding of how UPI works begins with the first crucial step: payer’s bank account verification. This digital handshake ensures that the person initiating the payment has sufficient funds, and it’s all done in real-time, thanks to the robust infrastructure provided by UPI.

The role of the National Payments Corporation of India (NPCI) and the unique UPI ID in securing transactions cannot be understated. These elements are fundamental to the secure, swift, and successful execution of every transaction, embodying the essence of how UPI works in maintaining the trust and safety of digital payments.

4. The Magic of Technology – How UPI Processes Payments

Delving into the heart of India’s digital payment revolution, the way UPI processes payments is akin to witnessing a magic show, where every act is meticulously planned and executed.

At the core of this magic is the UPI infrastructure, comprising banks, the National Payments Corporation of India (NPCI), and various payment service providers (PSPs).

An understanding of how UPI works in this context requires a look at the seamless collaboration between these entities.

Explaining the UPI Infrastructure: Banks, NPCI, and Payment Service Providers

- Banks: They hold the customer’s accounts, ensuring funds are available and secure for transactions.

- NPCI: Acts as the central authority that oversees UPI, ensuring all transactions comply with the necessary standards and regulations.

- Payment Service Providers (PSPs): These are the interfaces (UPI apps) that users interact with to initiate transactions.

Table 1: Roles and Responsibilities in UPI Infrastructure

| Entity | Role in UPI |

|---|---|

| Banks | Validate account details and fund availability; facilitate fund transfer. |

| NPCI | User interface for transaction initiation, linking bank accounts to UPI IDs, and providing transaction status. |

| PSPs (Apps) | User interface for transaction initiation, linking bank accounts to UPI IDs, providing transaction status. |

Real-time Processing: The Journey of a Digital Payment

- Transaction Initiation: A user initiates a transaction by entering the recipient’s UPI ID and the amount.

- PSP to Bank Communication: The PSP app communicates the transaction details to the payer’s bank.

- NPCI’s Role: NPCI routes the transaction details from the payer’s bank to the recipient’s bank, verifying the UPI IDs and transaction amounts.

- Fund Transfer: Upon validation, the recipient’s bank credits the amount, completing the fund transfer process.

Chart: Flow of a UPI Transaction

User (Payer) -> PSP App -> Payer's Bank -> NPCI -> Recipient's Bank -> User (Payee)

This real-time processing is what powers the “magic” of UPI, allowing for instant transfers that revolutionize how people transact daily.

5. Behind the Scenes – Security and Encryption in UPI Transactions

The security and encryption protocols within UPI act as the guardians of every transaction, ensuring user funds are always protected. This layer of security is what makes trusting UPI with your money easy.

Encryption: The Guardian of Your UPI Transactions

UPI uses end-to-end encryption to safeguard data transmission between all parties involved. This means that from the moment a user initiates a transaction, all information is encrypted, making it unreadable to anyone except the intended recipient.

Multi-layered Security: How UPI Protects Your Money

- Device Binding: Ensures the UPI app is tied to a specific device, adding an extra layer of security.

- Two-Factor Authentication: Combines something the user knows (PIN) with something the user has (mobile phone).

- Dynamic Encryption Keys: Each transaction is encrypted with a unique key, making it virtually impossible to intercept and decode.

Table 2: UPI’s Multi-Layered Security Features

| Security Feature | Description |

|---|---|

| End-to-End Encryption | Encrypts data transmission, ensuring privacy and security. |

| Device Binding | Links the UPI app to a specific device for an added security layer. |

| Two-Factor Authentication | Requires PIN and the device, enhancing security. |

| Dynamic Encryption Keys | Uses unique encryption for each transaction, preventing data breaches. |

6. The Conductor’s Baton – The Role of NPCI in UPI Transactions

The National Payments Corporation of India (NPCI) is akin to the conductor of an orchestra, ensuring each component of the UPI system works in harmony to create a seamless transaction experience. As the architect of UPI’s seamless transactions, NPCI plays several critical roles:

- Regulatory Oversight: NPCI sets the rules and standards for UPI transactions, ensuring they are secure, efficient, and accessible.

- Transaction Processing: It processes millions of transactions daily, routing them from the sender’s to the receiver’s bank.

- Innovation and Upgrades: NPCI continuously innovates, adding new features and capabilities to keep the UPI platform ahead of technological advancements.

Ensuring Smooth Operations in the UPI Ecosystem

NPCI’s role in ensuring smooth operations within the UPI ecosystem cannot be overstated. It uses sophisticated technologies and protocols to monitor transactions, manage risks, and prevent fraud, thus maintaining the trust and confidence of millions of users.

By overseeing the intricate dance of digital payments, NPCI not only ensures how UPI works remains a marvel of financial technology but also paves the way for future innovations that will continue to transform the landscape of digital payments in India and potentially around the world.

7. The Crescendo – Funds Transfer and Settlement

As we delve deeper into understanding how UPI works, the crescendo of the process—funds transfer and settlement—showcases the efficiency and speed of UPI transactions. From the moment the “Pay Now” button is pressed, to the funds landing in the recipient’s account, the journey is nothing short of digital wizardry.

From Payer to Payee: The Route of Your Money

The path your money takes from your account to the recipients involves several key players working in concert. When a transaction is initiated, it is completed immediately, typically within a few seconds, using the UPI platform, which is supervised by the NPCI. This real-time processing ensures that transactions, regardless of their size, are completed swiftly.

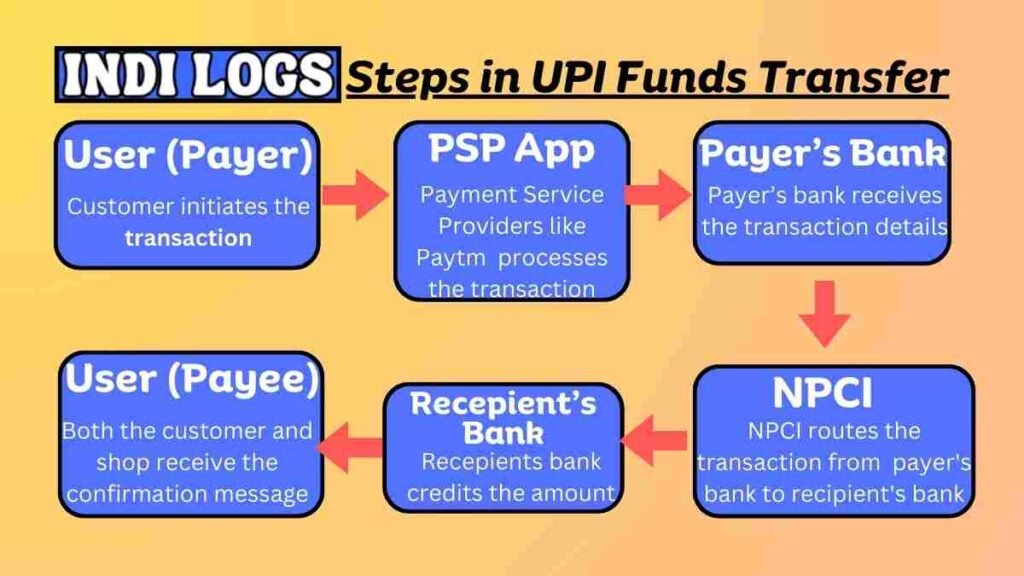

Table: Steps in UPI Funds Transfer

| Step | Action | Description |

|---|---|---|

| 1 | Transaction Initiation | The recipient’s bank credits the account. |

| 2 | PSP Processing | App processes transactions and forwards them to the payer’s bank. |

| 3 | NPCI Facilitation | NPCI routes the transaction to the recipient’s bank. |

| 4 | Funds Settlement | Recipient’s bank credits the account. |

| 5 | Transaction Confirmation | Both payer and payee receive notification of the successful transaction. |

Instantaneous Magic: How Funds Appear in the Recipient’s Account

The instantaneous appearance of funds in the recipient’s account is facilitated by UPI’s robust infrastructure and the seamless coordination between banks and NPCI. This “magic” is the result of sophisticated algorithms and secure communication channels that prioritize speed and security, making the process of how UPI works a marvel of modern fintech.

The Ovation – Confirmation of Transaction

The final act in the UPI transaction process is the confirmation of the transaction. This stage is crucial for both the payer and the payee, assuring that the transaction has been successfully completed.

The Final Act: Receiving the Success Notification

Upon successful completion of a transaction, UPI sends a confirmation notification to both the payer and the payee. This notification serves as an official record of the transaction, providing details such as the transaction amount, the recipient’s name, and the date and time of the transaction.

The Store Owner’s Perspective: Confirmation of Funds Received

For store owners and merchants, the confirmation of funds received is the moment of truth. This not only signifies the successful sale of goods or services but also the efficiency and reliability of UPI as a payment method. The instant confirmation allows businesses to operate smoothly, enhancing customer trust and satisfaction.

8. Troubleshooting – When Things Don’t Go as Planned

Despite the efficiency of UPI, there are times when transactions may not go as planned. Understanding how UPI works includes knowing how to address these hiccups.

Common Hiccups in UPI Transactions and Their Solutions

Some common issues include transaction failures, delayed settlements, and incorrect transaction amounts. Solutions typically involve checking network connectivity, verifying account balances, and ensuring correct UPI IDs are used.

Table: Common UPI Issues and Solutions

| Issue | Solution |

|---|---|

| Transaction Failure | Check network connectivity, try again later. |

| Delayed Settlement | Wait for a few minutes; delays are often short-lived. |

| Incorrect Amount Sent | Verify the amount before sending; contact customer support if an error occurs. |

The Role of Customer Support in Resolving Issues

Customer support plays a vital role in resolving issues when transactions don’t proceed as expected. Most UPI apps provide in-app support or helplines to assist users. Effective problem resolution not only ensures user satisfaction but also maintains the integrity and trust in the UPI ecosystem.

Both the banks involved and the NPCI provide channels for grievance redressal, ensuring users have recourse in case of issues.

- Customer Support Channels: Banks and PSPs offer 24/7 customer support via phone, email, and in-app support.

- NPCI Helpline: For unresolved issues, NPCI provides a helpline and an online complaint form for further assistance.

The understanding of how UPI works, including its mechanisms for funds transfer, confirmation, and troubleshooting, provides a comprehensive view of this revolutionary payment system. Its efficiency, combined with robust security measures, makes UPI a cornerstone of India’s digital economy, setting a benchmark for digital payments worldwide.

9. The Future of UPI – What Lies Ahead

As we peer into the horizon, the future of UPI looks as bright as the constellation in a clear night sky. Understanding how UPI works today lays the groundwork for appreciating the potential transformations it’s poised to bring to the global payment landscape.

The innovation and inclusivity driving UPI’s growth signal a new era of financial transactions that transcend borders.

Emerging Trends and Future Technologies in UPI

Emerging trends and the integration of cutting-edge technologies fuel the continuous evolution of UPI. Here’s a glimpse into what the future holds:

- Blockchain Integration: Leveraging blockchain technology could enhance UPI’s security, making transactions more transparent and tamper-proof.

- Cross-border Transactions: Efforts are underway to facilitate cross-border payments through UPI, potentially revolutionizing international trade and remittances.

- Integration with IoT Devices: As the Internet of Things (IoT) becomes more prevalent, UPI could be integrated with IoT devices for even more convenient payment options.

The Potential for UPI in Transforming Global Payments

The interoperability and instant payment features of UPI have the potential to make it a preferred platform for global transactions. By simplifying the payment process and making it more secure, UPI can offer a compelling alternative to traditional banking and payment systems worldwide.

Conclusion

Reflecting on the journey from initiating a UPI transaction to its successful conclusion, it’s clear that UPI is more than just a payment system; it’s a symphony of technology, security, and convenience.

This symphony, orchestrated by NPCI, showcases India’s prowess in digital innovation and its commitment to financial inclusivity. Understanding how UPI works is not just about comprehending a payment mechanism but appreciating a vision that has the power to transform the financial landscape globally.

FAQ’S Section

Q1: Is UPI safe for large transactions?

A1: Absolutely. UPI employs robust encryption and security protocols, making it safe for transactions of any size.

Q2: Can UPI be used for international payments?

A2: As of now, UPI is primarily used within India. However, there are plans to expand its functionality to support international transactions, showcasing the global potential of UPI.

Q3: What happens if I enter the wrong UPI ID?

A3: Funds transferred to the wrong UPI ID cannot be automatically reversed. It’s crucial to double-check the UPI ID before confirming a transaction. In case of a mistake, you should contact your bank or use the complaint mechanism within your UPI app.

Q4: How does UPI handle transaction failures?

A4: In case of a transaction failure, the deducted amount is typically refunded to the payer’s account within a few minutes to a few days. If the issue persists, contacting customer support is advisable.

Q5: Can I use UPI without a bank account?

A5: No, a bank account is necessary to use UPI, as it links directly to your account for facilitating transactions.

Understanding how UPI works, along with its current capabilities and future potential, not only provides insights into a revolutionary payment system but also highlights India’s role as a global leader in digital finance innovation.