{kind=link}

Table of Contents

Remember the reverence we once had for the neighbourhood ATM? It was a magical box, a symbol of progress and financial autonomy. Finding one with “No Cash” plastered on its screen was a minor tragedy, while discovering a working, air-conditioned kiosk felt like finding an oasis in the desert. The security guard stationed outside was a local landmark. That humble machine was our portal to “Any Time Money.”

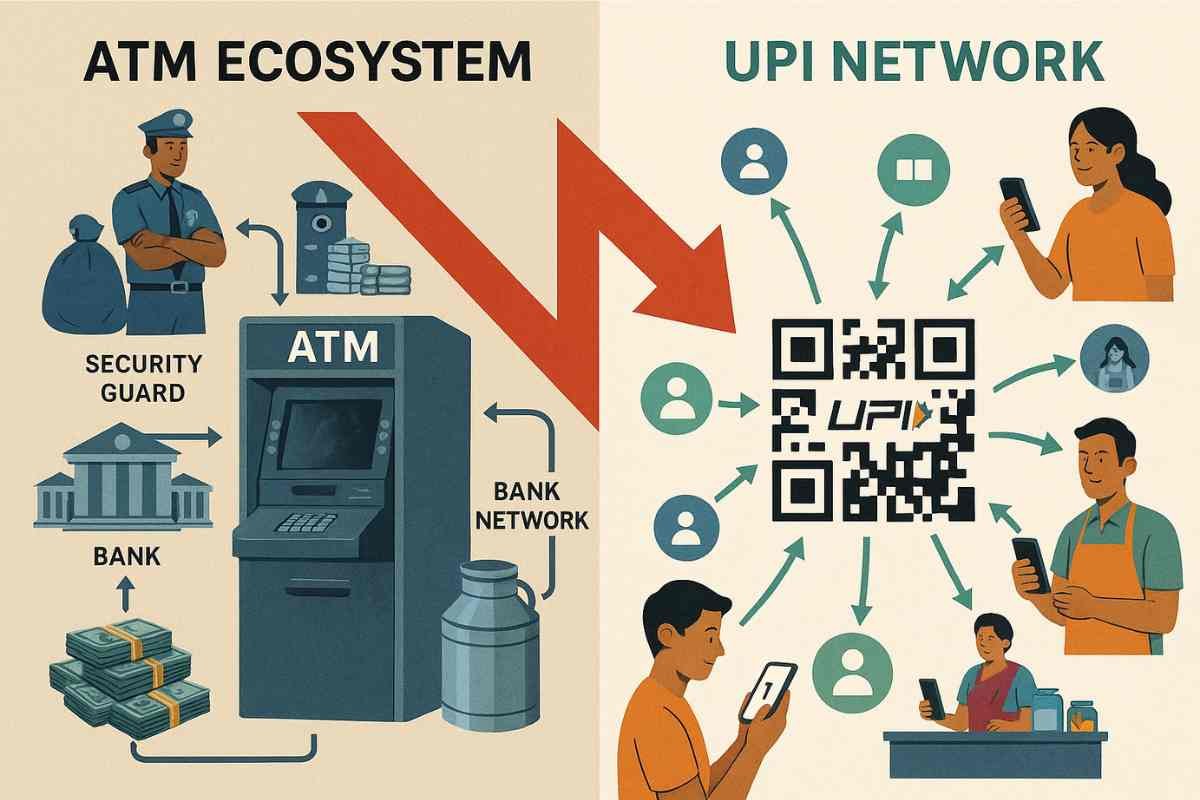

Today, that same box sits on the street corner, often ignored, increasingly derelict, its screen dark. Its slow, silent death is one of the most significant, yet uncelebrated, consequences of India’s digital leap of faith. The Unified Payments Interface (UPI) didn’t just create a new way to pay; in its phenomenal success, it accidentally signed the death warrant for the Indian ATM industry, triggering a great cash infrastructure collapse that is reshaping our relationship with money itself.

The Reign of the ATM: A Recent Memory

It feels like a lifetime ago, but it was just over a decade back that the expansion of the ATM network was a national mission. Banks competed to place their machines on strategic corners, and the number of ATMs was a key metric of financial inclusion. For millions, it was the first real taste of 24/7 banking. It liberated us from the tyranny of banking hours, long queues, and the tedious process of withdrawing cash from a teller.

The ATM was the undisputed king of convenience. Every festive season, every long weekend, was preceded by a collective national pilgrimage to these machines to stock up on cash. It was an entire ecosystem, employing lakhs of security guards, cash-in-transit staff who braved city traffic in armoured vans, and technicians who kept the machines running. It was a physical, tangible, and indispensable part of India’s economic landscape.

The Silent Coup: A QR Code Changes Everything

The revolution that toppled this kingdom didn’t arrive with a bang. It arrived with a beep. UPI wasn’t launched as an “ATM killer.” It was launched to solve a different problem: the friction of moving money between bank accounts. But its design was pure genius. It was free, instantaneous, and ridiculously easy to use.

Slowly at first, then all at once, the logic of our financial lives began to flip. The primary goal was no longer to withdraw cash to spend. The goal was to spend directly from your bank account. Why withdraw ₹500 from an ATM to pay a series of small vendors when you could just scan a QR code at each one? The chai wallah, the auto-rickshaw driver, and the kirana store—the very reasons we needed a constant supply of loose cash—were now nodes on the UPI network.

Convenience was redefined. It was no longer about having cash in your pocket; it was about having your entire bank balance accessible on your phone. UPI didn’t just compete with the ATM; it made the ATM’s core purpose redundant for a huge chunk of daily transactions.

The Economics of a Dying Giant

For the companies that run these ATM networks, this user behaviour shift has been catastrophic. An ATM is not just a machine; it’s a miniature, high-maintenance business. Consider the brutal economics:

- Crushing Operating Costs: An ATM incurs fixed monthly expenses: rent for the physical space, electricity (especially for the AC), security guard salaries, maintenance contracts, and software licenses. On top of this is the massive variable cost of cash logistics—transporting currency in secure vans, insuring it, and paying staff to load it. The average cost to run a single ATM can range from ₹75,000 to ₹1 lakh per month.

- Plummeting Revenue: The primary revenue for ATM operators is the “interchange fee” (around ₹17 per cash transaction) paid by a customer’s bank when they use another bank’s ATM. As people flocked to UPI, the number of transactions per ATM plummeted. With revenues crashing and fixed costs remaining high, the business model began to bleed profusely.

The data tells a stark story. After years of double-digit growth, the number of ATMs in India has stagnated and even started to decline. According to RBI data, the number of ATMs peaked and has seen a marginal decrease in recent years. The Confederation of ATM Industry (CATMi) has repeatedly raised alarms, stating that nearly half of India’s ATMs could become unviable and shut down if the economic model isn’t revised. It’s a classic squeeze: regulatory mandates for enhanced security (like cassette swap mechanisms) pushed costs up, while UPI pulled revenues down.

The Paradox of Progress: An Uneven Collapse

This collapse, however, is not uniform. In metros and Tier-1 cities, where smartphone penetration and data connectivity are high, the ATM is fast becoming a relic. But in rural and semi-urban India, the story is more complex. Cash remains king, digital literacy is a work in progress, and network connectivity can be patchy.

Herein lies the paradox: the very success of UPI, driving ATM unviability in cities, is causing operators to pull out of less profitable semi-urban and rural areas. This risks leaving a significant portion of the population with less access to cash, potentially harming the cause of financial inclusion. The digital wave that lifted millions in the city could leave others stranded on cashless islands.

It’s a curious case where the cash in circulation in the economy, as per RBI, remains high. This suggests that people still trust and hold cash for larger transactions or as a store of value, but its use as a high-frequency medium of exchange for small payments has been decimated by UPI.

Conclusion: The End of an Era, Not the End of Cash

The slow death of the ATM was an accident. No one at the NPCI or in the finance ministry set out to destroy the cash machine industry. They set out to build a world-class digital payment system, and they succeeded beyond their wildest dreams. The ATM industry became the collateral damage of that spectacular success—a textbook case of disruptive innovation.

What does the future hold for those empty boxes? They won’t vanish overnight. The ATM will likely evolve. We are already seeing a rise in Cash Recycler Machines (CRMs), which can both dispense and accept cash, turning them into mini-bank branches for deposits. They might morph into sophisticated “Digital Kiosks” offering a suite of banking services beyond just cash.

But the era of the simple cash dispenser as a central pillar of our financial lives is over. Its demise is a testament to India’s dizzying pace of change. So the next time you walk past a dark, silent ATM, take a moment. You’re not just looking at an obsolete machine; you’re looking at a monument to a revolution that changed the way a billion people think about money.

Call to Action:

When was the last time you hunted for an ATM? Has UPI completely replaced cash in your life? Share your experiences in the comments below! Pass this story on to anyone who remembers the good old days of “Any Time Money” and follow IndiLogs for more deep-dives into India’s economic transformation.