{kind=link}

Table of Contents

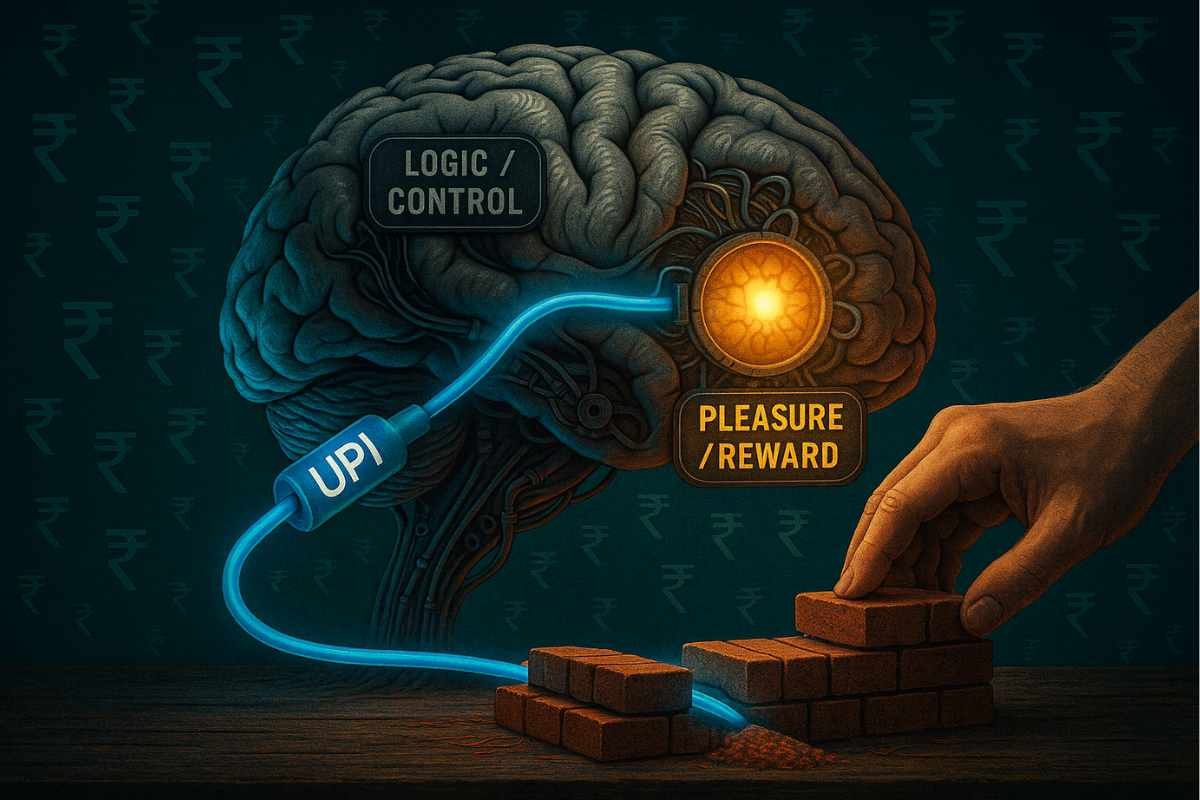

Let’s admit a hard truth: we are never going back. The days of stuffing thick wads of cash into a leather wallet, fighting for chutta (change) with an auto driver, or standing in line at an ATM to withdraw money for the week are over. The Unified Payments Interface (UPI) hasn’t just replaced cash; it has made it obsolete. But in this transition, something invisible and vital has been lost. We have lost the psychological “pain of paying”—that visceral, gut-check moment that happens when you physically hand over money. Our brains have been rewired. We now perceive spending money as a low-stakes, frictionless video game where the points (our bank balance) just go down, and we get the loot (the goods).

Acknowledging this isn’t luddism; it’s realism. We cannot reverse this psychological shift, but we can’t afford to let it ruin us either. If we are to survive and thrive in this digital economy, we need a new operating system for our minds. We need to artificially re-introduce friction. We need to build “digital speedbumps.” Here are seven practical techniques to protect your changed spending psychology and maintain discipline in a world designed to make you spend.

The Acceptance Phase: You Are a Digital Cyborg

First, stop beating yourself up for being “bad with money.” You aren’t bad with money; you are a human being with a stone-age brain trying to navigate a space-age financial system. Your brain was evolved to value tangible resources (food, shelter, physical coins). It was not evolved to process the abstract concept of a four-digit PIN code representing your life’s labor. Once you accept that the technology is actively exploiting your psychology, you can start building defenses.

1. The ‘Digital Air-Gap’ Strategy (Two Accounts)

The Psychology: When your UPI app is linked directly to your salary account, you are effectively walking around with your life savings in your pocket, ready to be spent on a samosa. The brain perceives the resource pool as “infinite” (or at least, very large), making small spends feel irrelevant.

The Technique: Open a secondary bank account (or use a digital bank). This is your “Spending Wallet.”

- The Action: On the 1st of the month, transfer your discretionary spending budget (e.g., ₹10,000) to this secondary account.

- The Rule: Link only this account to your primary UPI app for daily scanning. Remove your salary account or hide it deep in the settings.

- The Result: When you open GPay, you don’t see ₹5 Lakhs; you see ₹4,000. This creates artificial scarcity. You will naturally spend less because your brain sees a smaller, finite resource pool.

2. The ‘App Burial’ Protocol

The Psychology: “Out of sight, out of mind.” App designers want their icon on your home screen to trigger the “cue-routine-reward” loop. The easier it is to open the app, the easier it is to spend.

The Technique: Make it annoying to pay.

- The Action: Remove your UPI apps from your home screen. Buried them inside a folder named “Finance,” inside another folder named “Tools.”

- The Result: That extra 3 seconds it takes to find the app acts as a “cognitive pause.” It breaks the autopilot mode. It forces you to think, “Do I really want to dig for the app to buy this random thing?” Often, the answer is no.

3. The ‘Loud’ Notification Hack

The Psychology: UPI is designed to be silent. A quick vibration, a soft ping, and it’s done. This silence contributes to “spending amnesia.” We need to make spending money “loud” again.

The Technique: Re-sensitize your brain to the outflow.

- The Action: Go into your bank settings and turn on SMS and Email alerts for every transaction, no matter how small. Then, set a specific, annoying ringtone for these SMS alerts.

- The Result: Every time you spend, your phone screams at you. Then, you get an email. Then, you get an SMS. This triple-notification forces you to acknowledge the transaction. It brings the “pain of paying” back from the dead.

4. The ‘Widget of Shame’

The Psychology: We avoid looking at our bank balance because it induces anxiety (the Ostrich Effect). But ignorance breeds irresponsibility. We need to confront the reality of our finances constantly.

The Technique: Visual accountability.

- The Action: Use a widget (from your bank app or a third-party expense tracker) that displays your current “Spending Wallet” balance right on your home screen.

- The Result: Every time you unlock your phone to check Instagram, you see your balance staring at you. If it’s dropping fast, you see it in real-time. You cannot hide from the math. It acts as a subconscious anchor, reminding you of your limits throughout the day.

5. The ‘Cost Per Hour’ Translation

The Psychology: We have lost the sense of value. Is ₹500 a lot? In the UPI era, it feels like nothing. We need to translate the abstract number back into something tangible: your time.

The Technique: The mental converter.

- The Action: Calculate your hourly wage. (Net Monthly Salary ÷ 160 hours). Let’s say you earn ₹500 an hour.

- The Result: Before scanning a QR code for a ₹1,500 dinner, pause and say: “This dinner costs 3 hours of sitting in traffic and dealing with my boss.” Suddenly, the price isn’t just a number; it’s a chunk of your life. This reframing often kills the impulse to spend on things that aren’t truly worth your labor.

6. The 24-Hour ‘Cart Quarantine’

The Psychology: UPI makes online shopping dangerous because it removes the “cooling off” period. Impulse buys happen in seconds.

The Technique: Artificial delay.

- The Action: For any non-essential purchase over ₹500, you are allowed to put it in your cart, but you are forbidden from paying for it for 24 hours.

- The Result: This period is the “Cart Quarantine.” 90% of the time, the dopamine rush of “wanting” fades within a few hours. When you come back the next day, you’ll likely look at the item and wonder, “Why did I want this?” and delete it. You satisfy the urge to “shop” without the consequence of “spending.”

7. The Manual Ledger (The ‘Muneem-ji’ Method)

The Psychology: Automated expense trackers are great, but they are passive. You don’t “feel” the tracking. Writing something down requires active cognitive engagement.

The Technique: Retro friction.

- The Action: Create a WhatsApp group with just yourself (or your spouse). Name it “Expense Ledger.” Every single time you make a UPI payment, you must immediately type the amount and the item into that chat. “₹40 – Chai,” “₹250 – Uber.”

- The Result: The act of typing it out forces you to process the spending. It also creates a running, searchable ticker of your habits. Scrolling up through that chat at the end of the week provides a shocking, unfiltered reality check of where your money went.

Conclusion: Mindful Modernity

We cannot turn back the clock. We are digital natives now, living in a cashless economy. But that doesn’t mean we have to be mindless consumers. By acknowledging that our psychology has changed, and by implementing these seven techniques, we can protect ourselves.

We can enjoy the speed of UPI without succumbing to the speed of debt. We can use the technology without letting the technology use us. It takes a little bit of jugaad and a little bit of discipline, but your future self—and your bank account—will thank you for it.

Call to Action:

Which of these techniques resonates with you? Are you brave enough to try the “Widget of Shame”? Share your own tips for maintaining digital discipline in the comments below. Forward this survival guide to your friend who is always “broke” by the 15th of the month, and follow IndiLogs for more strategies on mastering the modern Indian life.