{kind=link}

Table of Contents

Step into any bustling Indian bazaar – the vibrant chaos of Crawford Market in Mumbai, the aromatic spice lanes of Khari Baoli in Delhi, or the flower-laden paths of Mallick Ghat in Kolkata. Amidst the cacophony of haggling voices and the kaleidoscope of goods, an intricate, often invisible, system of commerce hums along.

This isn’t just about cash changing hands; it’s built on generations of relationships, community reputation, and unique trust mechanisms like the khata (ledger) system and informal credit (udhaar).

Now, observe the ubiquitous QR codes plastered on even the smallest vendor stalls, the chaiwallah accepting instant digital payments, and the kirana store owner managing dues via a simple app. This isn’t a random adoption of technology; it’s a profound testament to how India’s traditional marketplaces, with their inherent systems of trust and high-volume, small-value transactions, have acted as powerful, culturally rooted catalysts for the fintech revolution, particularly in digital payments.

While Silicon Valley theorised about frictionless payments, India’s bazaars were already practising a version of it, albeit analog. The leap to digital wasn’t about reinventing commerce but about streamlining and scaling these deeply ingrained practices.

The genius of Indian fintech, especially platforms like UPI (Unified Payments Interface), lies in its ability to mirror the speed, low cost, and trust dynamics of the traditional bazaar, making the transition feel intuitive, almost natural, for millions of merchants and consumers. It’s a story of ancient commercial wisdom finding its most potent expression through modern code, proving that the future of finance in India is often coded in the customs of its oldest marketplaces.

The Bazaar Protocol: More Than Just Buying and Selling

To understand why bazaars are fintech nurseries, we need to appreciate their unique operational DNA:

- High Volume, Low Margins: Millions of small-ticket transactions happen daily. Profits often depend on volume, not high individual markups.

- The Power of Relationships: Regular customers and familiar vendors often operate on a relational basis. Your local subziwala knows your preferences; you trust his quality. This relationship often extends to informal credit.

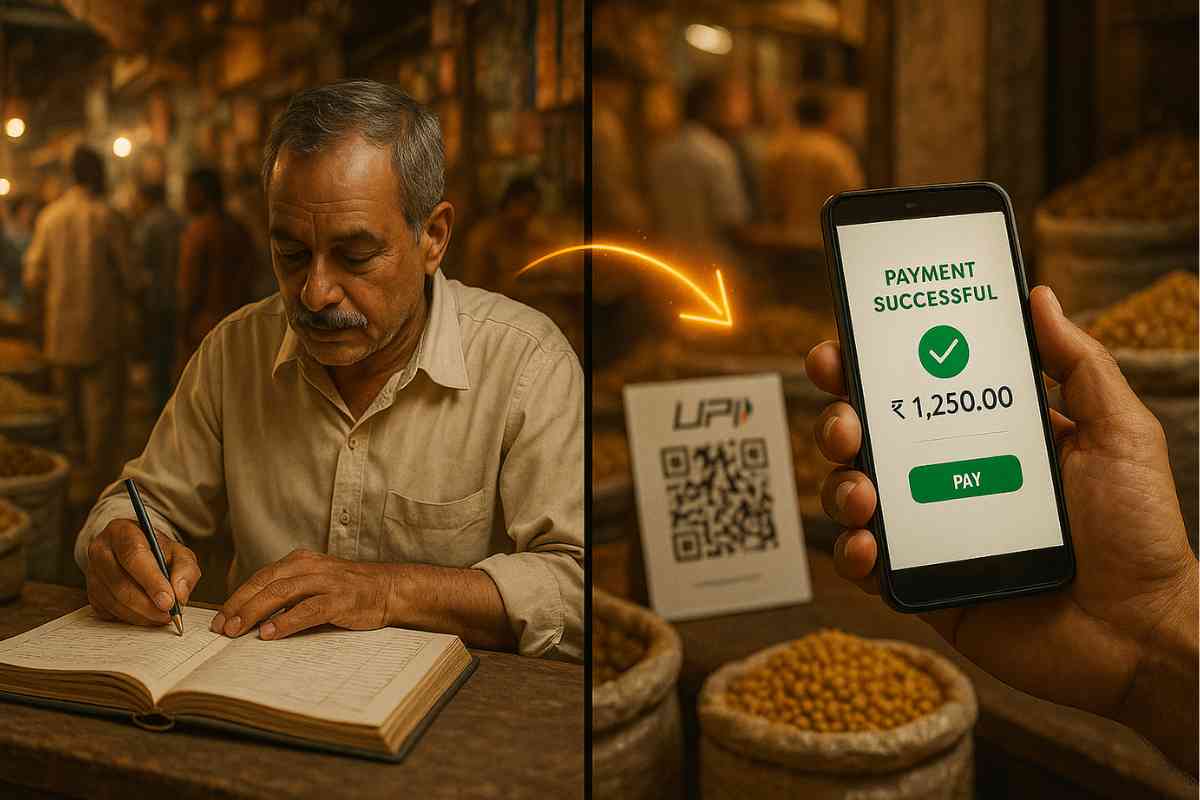

- The Ubiquitous Khata (Ledger): For centuries, the simple notebook or khata has been the backbone of credit in Indian commerce. Shopkeepers extend credit to known customers, meticulously recording dues. This system is built purely on trust and the understanding of eventual repayment.

- Community as Collateral: Reputation within the local community or market association often acts as a form of collateral. A default could mean loss of face and business, a powerful deterrent.

- Speed and Fluidity: Transactions are quick. Haggling is swift. Cash (traditionally) moves fast. There’s little patience for clunky processes.

- The Ecosystem of Interdependence: Wholesalers give credit to retailers, who give credit to consumers. It’s a chain of trust, enabling the flow of goods and services.

These elements created a commercial environment that, while heavily reliant on cash, already possessed sophisticated, albeit informal, systems for managing credit, trust, and high-frequency exchange.

From Galla Box to QR Code: How Fintech Mirrored Bazaar Dynamics

When digital payment solutions, particularly UPI, arrived, they didn’t force an alien system onto these bazaars. Instead, they offered a digital upgrade to existing practices:

- Zeroing in on Transaction Costs: A major barrier for digital payments globally has been Merchant Discount Rate (MDR) – fees merchants pay for transactions. For small bazaar vendors operating on razor-thin margins, this was a non-starter. UPI’s initial zero-MDR regime (and subsequent low-cost structure) was revolutionary. It mirrored the ‘costlessness’ of cash transactions, making it instantly viable for the smallest vendors. Paying for a ₹10 chai via UPI incurred no extra cost for the vendor or customer, a game-changer.

- Instant Gratification, Digital Confirmation: Bazaar transactions are immediate. UPI payments are real-time, with instant SMS or in-app confirmations for both parties. This immediate settlement and verification built trust rapidly, mimicking the certainty of receiving physical cash.

- Digitising the Khata – The Rise of Ledger Apps: Apps like Khatabook, OkCredit, and Vyapar digitally replicated the traditional khata. Shopkeepers could now record credit, send automated payment reminders via WhatsApp, and track dues digitally. This wasn’t replacing the trust system; it was making it more efficient, transparent, and easier to manage. It resonated because it solved a real, existing pain point using a familiar concept.

- Accessibility and Simplicity: A simple QR code and a basic smartphone were all that was needed. The learning curve was relatively gentle, aided by peer-to-peer learning within market communities. The “soundbox” providing audible payment confirmations further simplified things for merchants managing multiple transactions.

- Leveraging Existing Banking Infrastructure: UPI was built on existing bank accounts. Users didn’t need to open entirely new wallets with unknown entities; they were transacting from the perceived security of their established banking relationships, facilitated by a government-backed entity (NPCI). This foundational trust was crucial.

Fintech succeeded not by imposing a top-down solution but by offering tools that aligned with the existing bottom-up commercial realities of the bazaar.

Trust in Transition: From Personal Bonds to Platform Reliance

The traditional bazaar operates on deeply personal trust. How does this translate to seemingly impersonal digital platforms?

- Network Effects & Social Proof: Seeing neighbouring vendors adopt and benefit from digital payments acted as powerful social proof. If your competitor, whom you’ve known for years, trusts it, it lowers your barrier to adoption.

- Reducing Cash-Related Risks: For vendors, digital payments meant less hassle handling physical cash, reduced risk of theft or counterfeit notes, and no more scrambling for exact change. These tangible benefits built practical trust in the system’s utility.

- Formalizing Transactions, Building Credit History: While initially about convenience, digital transactions create a formal record. This is slowly helping small merchants build a digital financial footprint, potentially opening doors to formal credit from banks and NBFCs in the future – a powerful incentive.

- The “Illusion” of Continued Personal Connection: While the transaction is digital, the interaction often remains personal. You still buy from your known vendor; UPI is just the payment method. The underlying relationship often endures.

The trust isn’t necessarily transferred wholesale to the platform itself as an abstract entity, but rather to its utility, reliability, and the endorsements from their trusted community network.

Demonetization: The Unintended Catalyst

While the foundations were being laid, the 2016 demonetisation event acted as a massive, albeit disruptive, catalyst. The sudden cash crunch forced millions of merchants and consumers to explore digital alternatives out of sheer necessity. Platforms like Paytm and later UPI saw explosive growth. While disruptive, it broke inertia and familiarised a vast population with digital payments almost overnight, accelerating a trend that might have otherwise taken years.

The Bazaar’s Gift to Fintech: Lessons in Scalability and Frugality

The Indian bazaar, with its sheer scale and demand for ultra-low-cost solutions, has arguably pushed Indian fintech to be incredibly innovative and frugal. Building solutions for a billion people, many with limited digital literacy and low transaction values, forces a unique kind of ingenuity – the jugaad spirit applied to high tech.

- UPI’s architecture: Designed for massive scale at minimal cost, it’s a global case study.

- QR Code Simplicity: The cheapest, most accessible way to initiate a merchant payment.

- Lite Apps & Vernacular Interfaces: Catering to diverse linguistic needs and low-spec smartphones.

These aren’t just tech features; they are responses to the ground realities of India’s commercial landscape, heavily influenced by the bazaar model.

The Future: A Digitally Woven Bazaar

The journey isn’t over. While digital payments are widespread, the full digitisation of bazaar commerce – inventory management, supply chain integration, access to formal credit based on digital transaction histories – is still evolving. Platforms like ONDC (Open Network for Digital Commerce) aim to further democratise e-commerce, potentially bringing even the smallest bazaar sellers into the broader digital marketplace on their own terms.

The Indian bazaar, often seen as a relic of the past, has proven to be a surprisingly potent incubator for the future of finance. Its enduring principles of community, trust, and high-velocity exchange provided the cultural blueprint. Fintech innovators, by understanding and digitising these principles rather than trying to overwrite them, unlocked a multi-billion dollar industry and transformed how India transacts. The rhythmic chaos of the bazaar didn’t just birth fintech; it infused it with a uniquely Indian resilience and relevance.

What are your observations of fintech adoption in local Indian markets? How have digital payments changed your interactions in traditional bazaars? Share your experiences and insights in the comments below! If this perspective resonated with you, please share it on social media and continue following Indilogs for more culturally rooted analyses of India’s business and tech landscape.

2 comments

[…] local kirana stores for deliveries. The local shopkeeper acts as the trust bridge. If you are a fintech app, employ local “mitras” (friends/agents) who can explain your product face-to-face. Even a […]

[…] Unified Payments Interface (UPI) and its integrated bill-splitting features have undoubtedly made life easier, but in the process, […]