{kind=link}

Table of Contents

Tucked away in every Indian neighbourhood, nestled between homes and amidst the daily hustle, lies a financial institution more accessible, more humane, and more vital to the community than many modern banks. It has no intimidating glass doors, no complex paperwork, and its services are entirely interest-free. This remarkable institution is your local Kirana store, and its most powerful financial tool is a simple, unassuming notebook – the khata.

This isn’t just a ledger for groceries; it’s the heart of an informal, trust-based credit system that underpins the economic resilience of millions.

Forget FinTech disruption and complex algorithms. The local kirana-wala (grocer) has been running a sophisticated system of micro-lending for generations, based not on credit scores, but on character, familiarity, and a deep sense of community interdependence. This isn’t just about selling goods on credit; it’s a social contract that enforces accountability and acts as a crucial safety net during tough times, positioning these small retailers as the unsung bankers of our neighbourhoods.

The Anatomy of the Khata: A System of Sophisticated Simplicity

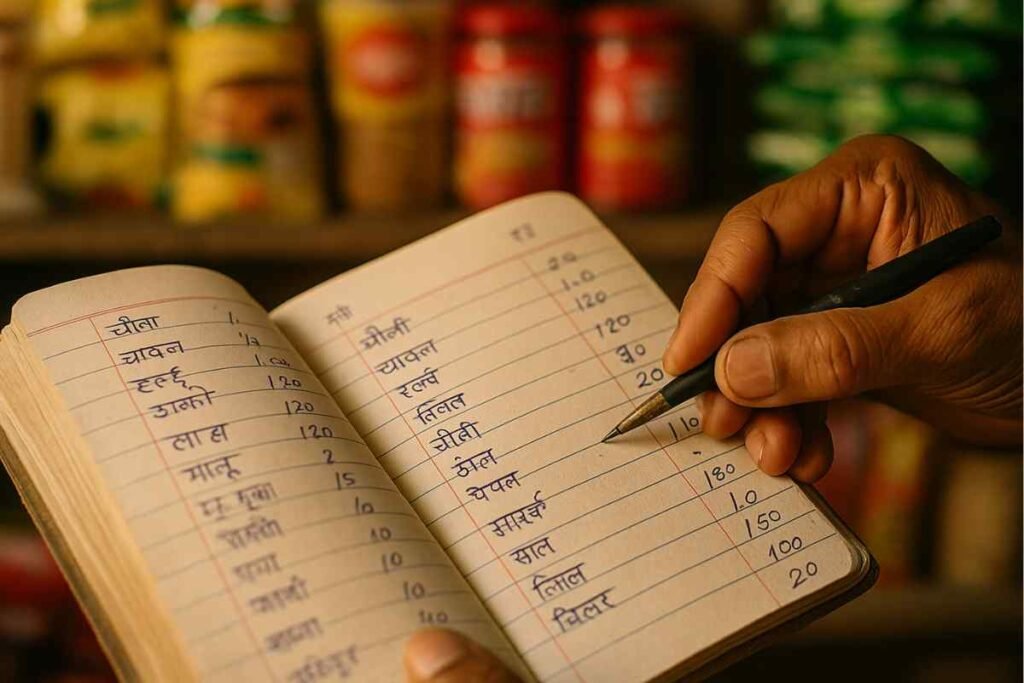

The khata system is beautifully, deceptively simple. It usually operates out of a dog-eared, long-format notebook, often with a faded cover depicting a deity or a scenic landscape.

- The Ledger of Lives: Each regular family in the neighbourhood has a designated page. Every time a purchase is made on credit – a litre of milk, a packet of biscuits, some onions and tomatoes – the date, the item, and the amount are meticulously handwritten by the shopkeeper.

- The Monthly Reckoning: There’s no fixed repayment schedule, no EMIs. The understanding, a gentle and unspoken one, is that the account will be settled periodically, usually when the family receives its monthly salary. This is often referred to as “clearing the khata.”

- The Currency of Trust: The most striking feature? There is zero interest charged. The credit is extended as a service, a gesture of goodwill to a loyal customer. The shopkeeper’s profit comes from the sale of goods, not from lending. The entire system operates on a currency far more valuable than rupees: mutual trust.

More Than a Grocer: The Kirana-Wala as Community Financier

By extending this informal credit, the kirana-wala takes on a role far beyond that of a simple retailer. They become a vital cog in the community’s financial machinery.

- The Ultimate Financial Shock Absorber: What happens when there’s an unexpected medical expense, a delay in salary, or a sudden job loss? The formal banking system might be unforgiving, but the khata at the local kirana store ensures that the family can still put food on the table. It acts as an immediate, accessible, and humane emergency fund for daily necessities, providing a crucial buffer during financial hardships.

- A Moral, Not Legal, Contract: The khata is not a legally binding document. There are no signed contracts or collateral. The system is upheld entirely by social accountability. A family that defaults on its khata doesn’t face legal action; they face the far more potent consequence of losing their good standing – their izzat (honour) – within the community. The shopkeeper knows them, their neighbours know them. This social pressure is often more effective than any legal threat.

- Credit Based on Character, Not Capital: A formal bank assesses you based on your income, your assets, your CIBIL score. The kirana-wala assesses you based on your character. Have you lived in the neighbourhood long? Are you known to be reliable? Do you pay your dues, even if sometimes delayed? This relationship-based assessment allows people who might be excluded from the formal credit system to access a lifeline.

The Unique Economics of Community Interdependence

This system creates a powerful, symbiotic relationship that defines the unique commercial ecosystem of Indian neighbourhoods.

- Ensuring Customer Loyalty: Why would a family travel to a large, impersonal supermarket that might offer a slightly better discount when their local kirana-wala trusts them enough to extend credit when they need it most? The khata system is the ultimate customer loyalty program. It creates a sticky, long-term relationship that big retail chains find almost impossible to replicate.

- Mutual Risk, Mutual Reward: The shopkeeper takes a risk by extending credit. However, this risk is mitigated by their deep knowledge of the community. In turn, the community supports the shopkeeper, ensuring their business remains viable. It’s a closed-loop system where everyone has a vested interest in the other’s well-being.

- A Precursor to Modern FinTech?: Interestingly, modern “Buy Now, Pay Later” (BNPL) services are essentially a digitised, monetized version of the khata system. But they lack its most crucial elements: the personal relationship, the community context, and the interest-free, humane flexibility.

A System Under Pressure, But Remarkably Resilient

In the age of instant UPI payments, massive e-commerce platforms, and express grocery delivery apps, is the humble khata becoming obsolete? Not by a long shot.

- Coexistence with Digital: Many kirana-walas have adapted brilliantly. They now accept UPI payments for immediate purchases while still maintaining the khata for their regular credit customers. The notebook might now be supplemented with a smartphone app, but the principle of trust-based credit remains.

- The Enduring Need for a Safety Net: As long as financial uncertainty exists, the need for a flexible, humane credit system for daily essentials will persist. The formal financial system cannot, and perhaps should not, fill this hyper-local, trust-based niche.

- The Human Touch: Ultimately, the khata system endures because it is fundamentally human. It recognizes that life is complicated, that salaries can be late, and that trust and relationships are the bedrock of a strong community.

The corner shop’s credit system is a quiet, powerful testament to the social intelligence and economic ingenuity embedded in Indian society. It’s a sophisticated financial institution masquerading as a simple grocery store, running on principles that prioritize community resilience over pure profit. It reminds us that sometimes, the most effective economic models aren’t found in business school textbooks but in a small, unassuming notebook, held in the trusted hands of your neighbourhood kirana-wala.

Does your family have a long-standing ‘khata’ with a local shopkeeper? What are your memories of this unique system of trust? Share your stories in the comments below!

Did this article give you a new appreciation for your neighbourhood grocer? Share it on your social media and celebrate this unsung hero of our communities!

Keep coming back to IndiLogs for more insightful explorations of the Indian experience.