{kind=link}

Table of Contents

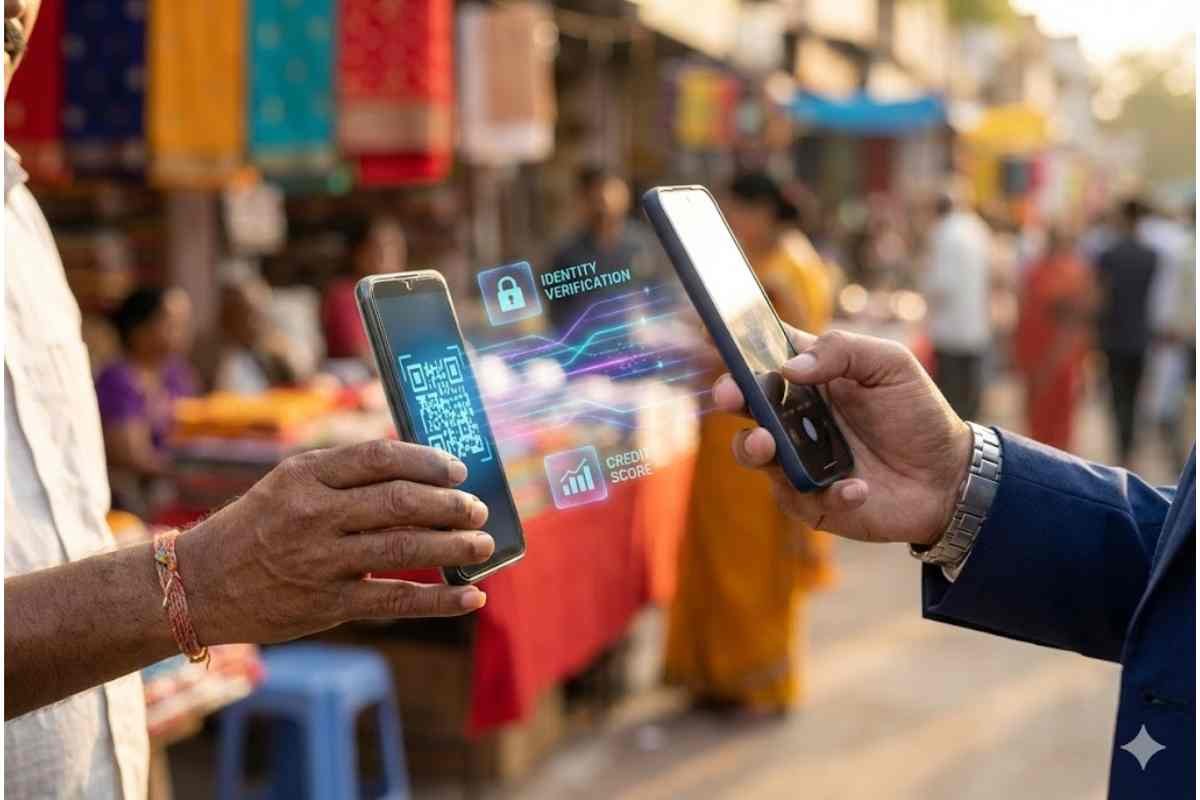

If you walk into a boardroom in San Francisco or London today, the topic of conversation often drifts, with a mix of awe and jealousy, to the “India Stack.” The world is watching in disbelief as a nation of 1.4 billion people leapfrogged credit cards and complex banking protocols to embrace a digital public infrastructure (DPI) that is arguably the most advanced on the planet. Yet, ironically, back home in our own offices in Mumbai, Bengaluru, and Delhi, many businesses still view this infrastructure merely as a “payment method.” We see the QR code on the sabziwala’s cart and think, “Convenient.” We don’t see the underlying rails that could skyrocket our business efficiency.

This is a massive missed opportunity. The Indian government has essentially built a free, high-speed digital highway. While global tech giants spend billions building proprietary walled gardens, India has democratised the very fabric of the digital economy—Identity (Aadhaar), Payments (UPI), Data (Account Aggregators), and Commerce (ONDC). This isn’t just “tech”; it is a public utility, as vital as electricity or roads.

For the Indian entrepreneur, this infrastructure is a cheat code. It allows a startup in Jaipur to verify a customer in Guwahati instantly for pennies, process their payments for free, and access their credit history securely. It collapses the cost of trust, the cost of transaction, and the cost of acquisition. If you are still treating UPI just as a way to save on card swiping fees, you are thinking too small. Here are five strategic ways to leverage India’s digital infrastructure to unlock explosive business growth.

1. Weaponise Frictionless Payments: UPI Autopay & The Subscription Economy

We all know UPI handles billions of transactions a month. But the real game-changer for business growth isn’t the one-time transfer; it’s UPI Autopay.

Historically, the “subscription economy” in India was strangled by the friction of standing instructions on credit cards (which few Indians have) or the nightmare of NACH mandates (paperwork that took weeks). UPI Autopay changes the physics of recurring revenue. It allows any business—from a SaaS platform to a milk delivery service to a gym—to set up recurring mandates under ₹15,000 instantly.

- The Strategy: Pivot your business model from transactional to recurring. If you sell consumables (coffee, supplements, stationery), offer a “Subscribe & Save” model powered exclusively by UPI Autopay. The friction of re-ordering is the biggest killer of Customer Lifetime Value (LTV). By locking in the mandate on a platform the customer trusts and uses daily, you secure cash flow and reduce churn. Don’t just ask for payment; ask for a relationship.

2. Slash Onboarding Costs with the ‘Identity Layer’ (e-KYC)

In the old days (read: five years ago), onboarding a customer for a regulated service like insurance, lending, or wealth management was a logistical horror show. It involved physical document collection, “wet signatures,” and a verification cost that could run upwards of ₹500 to ₹1000 per customer. This high Customer Acquisition Cost (CAC) made it impossible to serve the “sachet” market—the customer who only wanted a ₹500 mutual fund or a ₹10,000 loan.

- The Strategy: Integrate Aadhaar e-KYC and DigiLocker into your onboarding flow. This brings the cost of verification down from hundreds of rupees to single digits. It turns a week-long process into a 30-second flow. This doesn’t just save money; it opens up entirely new markets. You can now profitably serve the Tier-3 customer because the cost of “trusting” them has vanished. If your signup process still asks a user to “upload a scan of your ID,” you are living in the past. Switch to a fetch-based API model where the user simply consents to share their verified data.

3. ONDC: Breaking the Duopoly and Going Hyper-Local

For years, if you wanted to sell online in India, you paid a “rent” (commission) of 20-30% to the big platform monopolies. You owned the inventory, but they owned the customer. Enter the Open Network for Digital Commerce (ONDC). It is not an app; it is a protocol. It allows a buyer on a generic app (like Paytm or PhonePe) to see products from a seller on a different seller app (like Magicpin or a dedicated Shopify plugin).

- The Strategy: Unbundle your logistics and your discovery. Get your catalogue listed on the ONDC network. This allows you to be discoverable by millions of users across multiple buyer apps without being beholden to the algorithms of a single giant marketplace. Use ONDC-integrated logistics partners to handle hyperlocal delivery at a fraction of the cost of building your own fleet. This is particularly potent for D2C brands and local retailers who can now compete on visibility with the giants.

4. The Account Aggregator (AA) Framework: Cash-Flow Based Lending

One of the biggest hurdles for B2B growth is working capital. Traditionally, getting a business loan meant pledging collateral (property/gold). But what about the service business with strong cash flows but no assets? Or the MSME with a thick order book but thin margins?

The Account Aggregator (AA) framework is the “Data Democracy” layer of the India Stack. It allows a business to securely share its financial data (GST returns, bank statements) with a lender digitally to get instant credit.

- The Strategy: If you are a B2B platform or marketplace, integrate AA to offer “Embedded Finance” to your partners. Don’t just be a supplier; be a banker. If you supply raw materials to small manufacturers, use their transaction history on your platform + their AA data to underwrite credit for them. You unlock their growth (by giving them capital to buy from you), and you create a sticky ecosystem where you are indispensable to their operations.

5. Bhashini: Breaking the Language Barrier with AI

We often forget that the “digital divide” in India is largely a linguistic one. The internet is English-first; India is not. Bhashini is the government’s AI-led language translation mission, aiming to build a national digital public platform for languages. It creates open-source datasets to train AI models in Indian languages.

- The Strategy: Use the APIs emerging from the Bhashini ecosystem to vernacularise your business at scale. If you are building a customer support bot, don’t build it from scratch. Leverage these public resources to build voice-first, vernacular interfaces. Allow a customer in rural Bihar to speak to your app in Bhojpuri, and have your system process it in English. This infrastructure allows you to access the “Next Billion Users” not just as a marketing slogan, but as a genuine, serviceable customer base.

The Public Road to Private Profit

The beauty of India’s digital infrastructure is that it is built as a public good, but it is designed for private innovation. It separates the “rails” (which should be a monopoly, like roads) from the “trains” (which should be competitive, like cars).

For too long, Indian businesses have tried to build their own private roads. We built clumsy proprietary wallets, expensive physical verification networks, and closed-loop loyalty systems. It’s time to stop paving your own driveway and start driving on the Autobahn the government has built. The businesses that win the next decade will be the ones that build on top of the India Stack, treating it not as government compliance, but as the ultimate competitive advantage.

Is your business fully integrated with the India Stack, or are you still relying on legacy systems? Which layer—Identity, Payments, or Data—do you find most powerful? Share your insights in the comments below!